Investors have always been attracted to companies which are cash generating machines. The reason is simple. The cash generators survive market cycles. They keep doling out huge cash in turn which is either re invested if the business is in growth phase or returned as dividends if the company is in mature phase and doesn’t needs cash for reinvestment. In both the cases its beneficial for the minority shareholders because internal accruals is the cheapest source of capital for a company to build a business while if free cash is given off as dividends or buybacks it puts money in hand of shareholders directly.

While the free cash generation capacity makes these business attractive there is an inherent risk which lurks which some investors fail to identify. Capital Allocation becomes very important for a company which is generating huge amounts of cash from its operations. The simple thing to do would be to keep re investing in the business but not all businesses are at similar stages of growth. Thus some companies choose to give off the money as dividends to shareholders. However, in a case where a company does not share cash with shareholders but re invests in its business it needs to be identified whether the business is/will be able to generate returns higher than opportunity cost of capital for shareholders. Many times companies have squandered cash from good business in bad business while showing it off as diversification. However it becomes difficult for an investor to differentiate between diversification and wasteful conglomerisation. The loser is the minority shareholder.

We can see the difference that capital allocation makes on returns for a shareholder

- ITC has grown market cap at a rate of 22 percent over a growth in reserves of 19% while VST Industries has grown market cap. at a rate of 26 percent with a much lower growth in reserves at 11 percent

- While ITC ploughs money from highly profitable ciggarate business into loss making hotels, early stage FMCG, agri operations etc VST follows a simple approach of paying off cash as dividends

- The difference in returns for a shareholder in VST and ITC are there to see

To put in simple words an investment of Rs 1 lakh made in ITC 14 years ago would have resulted in Rs 16.55 lakhs while a similar amount invested in VST Industries would have resulted in Rs 25.5 lakhs. That is a difference of over 50 percent on the final amount. This is why capital allocation is important for companies and also for investors

Over the last few months a new space that has seen much action in the recent times, one due to inflow of money by domestic investors which has made the “assets under management” (AUM) touch new highs everyday while next due to the listing of one of the biggest companies in the asset management space – Reliance Nippon Asset Management Co. (RNAM) is the “Asset Management” industry.

The point that catches our eye in this industry is the ability to generate large amounts of cash flow and minimal use of capital to grow this business. This is a combination which will allow companies in this space (especially leaders) to generate large amounts of cash. We find this business to be very interesting because capital allocation will become very important when you have large amounts of idle cash. It is a great way to test management honesty and acumen.

We have already seen how capital allocation of management decides what will future returns are from a cash generator. Thus now let us have a look at how two companies in the AMC sector operate and let’s understand how they are allocating capital for themselves and their shareholders

Motilal Oswal is a diversified financial conglomerate with varied interests in the areas of broking, asset management and housing finance. On the other hand, Reliance Nippon is a pure play Asset Management Company with a host of offerings that include mutual funds(both debt and equity) , Alternative Investment funds and Portfolio Management services for both individuals and institutions

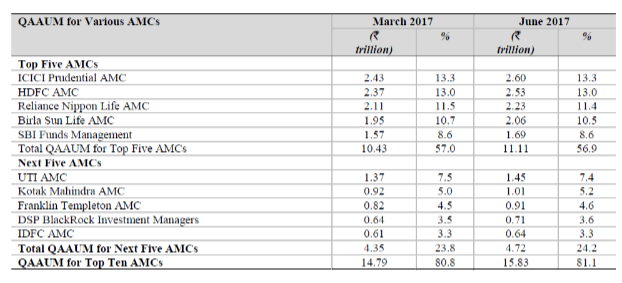

First we would like to give some facts about the AMC industry in India

- There are 41 AMC’s in the country, of which 9 are owned by government, 7 by foreign and 25 domestic private institutions

- Five of the top AMC’s control 57 percentage of the market with 36 accounting for the rest

Now we start our exercise in understanding the fund structure and capital allocation policies which both Reliance AMC & Motilal Oswal following terms of deploying the windfall that they get in terms of free cash.

Reliance AMC

To understand the implication of capital allocation policies, let us first look at the difference between core business pre-tax RoE's. The pre tax RoE in this case is equal to the PBT + unrealized income on investments divided by average equity

The profit before tax includes the component of other income which should be subtracted to understand core business RoE's. Similarly, the denominator should be reduced by the amount of interest/income earning assets that the company has invested into. The excel attached below shows the calculation for the same

Thus core ROE’s of AMC business which Reliance operates is on an average over 100% every year which portrays the operational strength of the industry in which it operates. The benefit of operating leverage once leadership position is established is enormous for the industry

Now to answer the question that why reported RoE's are so depressed in relation to core business RoE's?

We listed down all the investments that the company had made from its internal accruals and calculated the subsequent returns earned. To not obscure our findings, we included both realized and unrealized gains that have accrued to the company

Observation

- The company practices a diversified approach to asset allocation

- The part that is worrying are the inter corporate deposits, more so because we know who the related party for Reliance AMC are

- Even though the fund house has a sizeable private equity corpus, the balance sheet doesn't seem to have any investments into them as of March 2017

- The returns for a shareholder of RAMC would depend upon asset allocation policies of the management

Motilal Oswal Financial Services (MOFS)

It would be imperative for the reader to understand that MOFS is a diversified financial services business with interests in the credit business as well. So in this regard, an apple to apple comparison is not possible. What needs to be done is that the consolidated balance sheet of the company must be looked at ex of the loans and advances made as they pertain to the housing finance business if one needs to compare yields that both companies are earning on their investments

We took the data of the last three years for Motilal AMC (as the mutual fund schemes were launched only in the year 2014) and tried understanding profitability trend through ROE since inception of the schemes (prior to the Mutual fund triumvirate, MO-AMC was a pure play portfolio management services firm with an AuM growth of 10.65 percent in 7 years)

Let us now look at the capital allocation policies of MOFS

Observation

- The company practices an approach which is highly tilted towards equities and real estate

- Amongst equities MOFS also runs a private equity business which allows an investor to take exposure in the highly lucrative private equity and venture capital space

- MOFS also runs a Real Estate fund which gives exposure to real estate opportunities arising in the country

Reliance AMC vs MOFS

- While MOFS is a firm specialized in one domain – equities Reliance MAC manages a diversified pool which includes debt assets as well where the yields are very low thus depressing yields

- While the clients of MOFS includes HNI’s interested in PMS and equity schemes Reliance AMC manages the corpus for EPFO & NPS pension scheme which carries virtually zero yields

Thus the capital allocation of MOFS is tilted towards only one domain ie. Equity while Reliance has diversified it across multiple asset classes and also there seems to be some unanswered inter corporate loans which warrants further attention.

good analysis. kudos......but was keenly coming towards end to know your final verdict but just ended like bahubali-1 ..so,do you reckon RNAM is best to play?

ReplyDeleteHi Senthil, this isnt an exercise in identifying the better investment here. What we've tried to do is just show how two coompanies in th esame line of business manage their windfall from business. Investing is a function of several moving parts and hence we refrain from giving out an investment recommendation per se.

DeleteWe arw with Dhruv Saraf. True We R long term investor with RIL our number of shares are increasing also getting supper divident. Overall RIL is available in our family portfolios. Thanks.

DeleteHello Everybody,

DeleteMy name is Ahmad Asnul Brunei, I contacted Mr Osman Loan Firm for a business loan amount of $250,000, Then i was told about the step of approving my requested loan amount, after taking the risk again because i was so much desperate of setting up a business to my greatest surprise, the loan amount was credited to my bank account within 24 banking hours without any stress of getting my loan. I was surprise because i was first fall a victim of scam! If you are interested of securing any loan amount & you are located in any country, I'll advise you can contact Mr Osman Loan Firm via email osmanloanserves@gmail.com

LOAN APPLICATION INFORMATION FORM

First name......

Middle name.....

2) Gender:.........

3) Loan Amount Needed:.........

4) Loan Duration:.........

5) Country:.........

6) Home Address:.........

7) Mobile Number:.........

8) Email address..........

9) Monthly Income:.....................

10) Occupation:...........................

11)Which site did you here about us.....................

Thanks and Best Regards.

Derek Email osmanloanserves@gmail.com

Hello Everybody,

My name is Ahmad Asnul Brunei, I contacted Mr Osman Loan Firm for a business loan amount of $250,000, Then i was told about the step of approving my requested loan amount, after taking the risk again because i was so much desperate of setting up a business to my greatest surprise, the loan amount was credited to my bank account within 24 banking hours without any stress of getting my loan. I was surprise because i was first fall a victim of scam! If you are interested of securing any loan amount & you are located in any country, I'll advise you can contact Mr Osman Loan Firm via email osmanloanserves@gmail.com

LOAN APPLICATION INFORMATION FORM

First name......

Middle name.....

2) Gender:.........

3) Loan Amount Needed:.........

4) Loan Duration:.........

5) Country:.........

6) Home Address:.........

7) Mobile Number:.........

8) Email address..........

9) Monthly Income:.....................

10) Occupation:...........................

11)Which site did you here about us.....................

Thanks and Best Regards.

Derek Email osmanloanserves@gmail.com

What about the theory of 'nurturing' emerging business within the overall company/corporate entity/structure. Has HDFC Ltd. (not HDFC Bank because most people confuse both as one entity) not "nurtured" its various businesses including insurance and AMC, etc.

ReplyDeleteYou can't be focussed in capital allocation when you are "nurturing" new and emerging businesses. And during that period, the returns would be low. At some appropriate time, when the new and emerging business stabilises, then, it will give huge return to the shareholders.

Hi Kamal,

DeleteThis would not apply to Reliance Asset as it really is a standalone AMC without any material subsidiary that it can grow( unlike HDFC which has the life insurance, general insurance and the AMC business)- so its internal accruals are all re-invested into its own mutual funds. The company really does not have an emerging business unlike Motilal which has reinvested its acrruals from the broking and AMC business into housing finance

Interesting analysis, I'm glad that I read it. However, I had some un/related questions:

ReplyDelete- How can you be so sure that the assets you removed from RNAM are non-operating? Generally a certain amount of cash/liquidity is needed for operations and a new entrant would have to invest in the same.

- I do not know the accounting conventions of AMCs, but I would imagine that many investment vehicles are off-balance sheet entities. i.e. if RNAM starts a private equity fund then it would have very little, maybe base investment, as a non-current asset. Is this accurate?

- Do financial regulations play any part in stipulating what investments can be held?

Also, in your comparison with ITC and VST, shouldn;t you compare the total returns to better capture the value of dividends that VST paid out? If your statement is true that VST paid its excess cash as dividends, its return would be much higher.

DeleteHi,

Deleteon your point of assets being off balance sheet, indeed they are. but if the company does invest some of its money into those funds, it has to be categorized as a non-current investment as is the case with Motilal

On the point of financial regulations, I am not too sure and there wasn't any mention of the same in the various documents that I have read. I will read further and get back on this point.

Lastly, an AMC is a people's business so to say, most of the operating assets would be the employees of the company . The company has a certain amount of its cash parked in FD's and certain part under current accounts and a basic understanding would tell us that cash under current accounts is what really would entail the basic capital needs of the company and that anyways doesn't fetch any returns.

Very interesting article to inhance a clear difference in two co.

ReplyDeleteAs an investor, the moment you invest your money - in whatever financial instrument you choose - you initiate your own personal investment portfolio. A 'good' investment portfolio as such is one containing a healthy mix of low risk, medium risk and high risk investments straddling various investment tools such as debt funds, stock and fixed income elements. O connor portfolio

ReplyDeleteThis is really very informative and very detailed blog. Thank you so much for sharing this post, Ir really helped me a lot to understand that what is inventory and strategy for it.inventory management marketing materials.DLXpress is Best Delivery Service in CA , USA . know more about me. visit here - www.dlxpress.com

ReplyDeleteThanks for Blog!

ReplyDeleteLoan Against Property in Gurgaon

Your new valuable key points imply much a person like me and extremely more to my office workers. With thanks; from every one of us.

ReplyDeletesafety course in chennai

Get a personal loan from €3, 000 to € 20, 000, 000 within 24 hours upon request. Other types of loans are also available in less than 72 hours. Contact me as

ReplyDeleteneeded. Contact Us At :clemalphafinance@gmail.com whatspp Number +91-8546023893

Mr. Clem Alpha

Business loan

Home loan

Debt consolidation loans

Student loan

Construction loan

Car loan

Hotel loan

Personal loan

Refinancing Loan

Farm Loan

Truck Loan etc.

ReplyDeleteAre you in need of a loan?

Do you want to pay off your bills?

Do you want to be financially stable?

All you have to do is to contact us for

more information on how to get

started and get the loan you desire.

This offer is open to all that will be

able to repay back in due time.

Note-that repayment time frame is negotiable

and at interest rate of3% just email us.

Email : clemalphafinance@gmail.com

call or add us on what's app +447541246028

call or add us on what's app +91-8546023893

ReplyDelete¿Necesita un préstamo rápido a largo o corto plazo con una tasa de interés relativamente baja tan baja como 3%? Ofrecemos préstamos comerciales, préstamos personales, préstamos para la vivienda, préstamos para automóviles, préstamos para estudiantes, préstamos para consolidación de deudas, etc. No importa su puntaje de crédito. Tenemos la garantía de brindar servicios financieros a nuestros numerosos clientes en todo el mundo. Con nuestros paquetes de préstamos flexibles, los préstamos pueden procesarse y transferirse al prestatario en el menor tiempo posible, comuníquese con nuestro especialista para obtener asesoramiento y planificación financiera. Si necesita un préstamo rápido, contáctenos en: correo electrónico: clemalphafinance@gmail.com Whats-app us on: +91-9818603391 Mr.Clem Alpha on: +91-9818603391 Mr.Clem Alpha

I like your blog. Your given post is very informative. Thanks for sharing. Moon Sun Industries offer Sugar Refinery Plant in Uttar Prades. We are a leading brand, known for the best manufacturers of Sugar Refinery Plant.

ReplyDelete